®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

30.4k

30.4k

Who is covered under e-invoicing from 01 Oct 2022?

All about e-invoice applicability from 01.10.2022.

Click here for e-invoice applicability calculator

Q) What is e-invoicing?

As per Rule 48(4) of CGST Rules, notified class of registered persons have to prepare invoice by uploading specified particulars of invoice on Invoice Registration Portal (IRP) and obtain an Invoice Reference Number (IRN).

After following above ‘e-invoicing’ process, the invoice copy containing the IRN (with QR Code) issued by the notified supplier to buyer is commonly referred to as ‘e-invoice’ in GST.

Q) Who is liable for e-invoicing?

Only whose taxpayers whose aggregate turnover exceeds the threshold limit are liable to generate e-invoice.

Q) What is the threshold limit for e-invoicing?

As per Notification No.13/2020 - CT, current threshold limit for e-invoice applicability is Rs. 20 Crores. However this limit has been reduced to Rs. 10 Crores w.e.f. 01st Oct 2022 vide Notification No.17/2022 - CT.

Q) Which year's turnover is to be checked for e-invoice applicability?

The threshold limit is to be checked for all preceding financial years starting from FY 2017-18. That means, if threshold limit exceeds in any of the Financial Year starting from FY 2017-18, then e-invoice will become applicable.

Please note that law states preceding financial year, that means current financial year turnover is not to be considered.

Q) Can an e-invoice be cancelled or modified?

An e-invoice cannot be modified directly. However it can be cancelled within 24 hours of the generation of the IRN.

Post completion of 24 hours, the supplier can issue either a debit note or credit note or edit Form GSTR-1 modifying the respective invoice details.

Cancellation of IRN is not possible in case the e-way bill is already generated / active for the respective IRN.

Once the e-invoice (IRN) is cancelled, the same invoice number cannot be re-used to generate another IRN.

Partial cancellation of e-invoice (i.e., IRN) is not possible. Full e-invoice has to be cancelled.

Q) Whether all entities are required to generate e-invoicing?

|

☛ Login to read more...

|

:

:

E-invoice

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 30 Sep, 2022 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Comments

Aug 18, 2022

Post your comment here !

|

Login to Comment

|

Other Important Updates

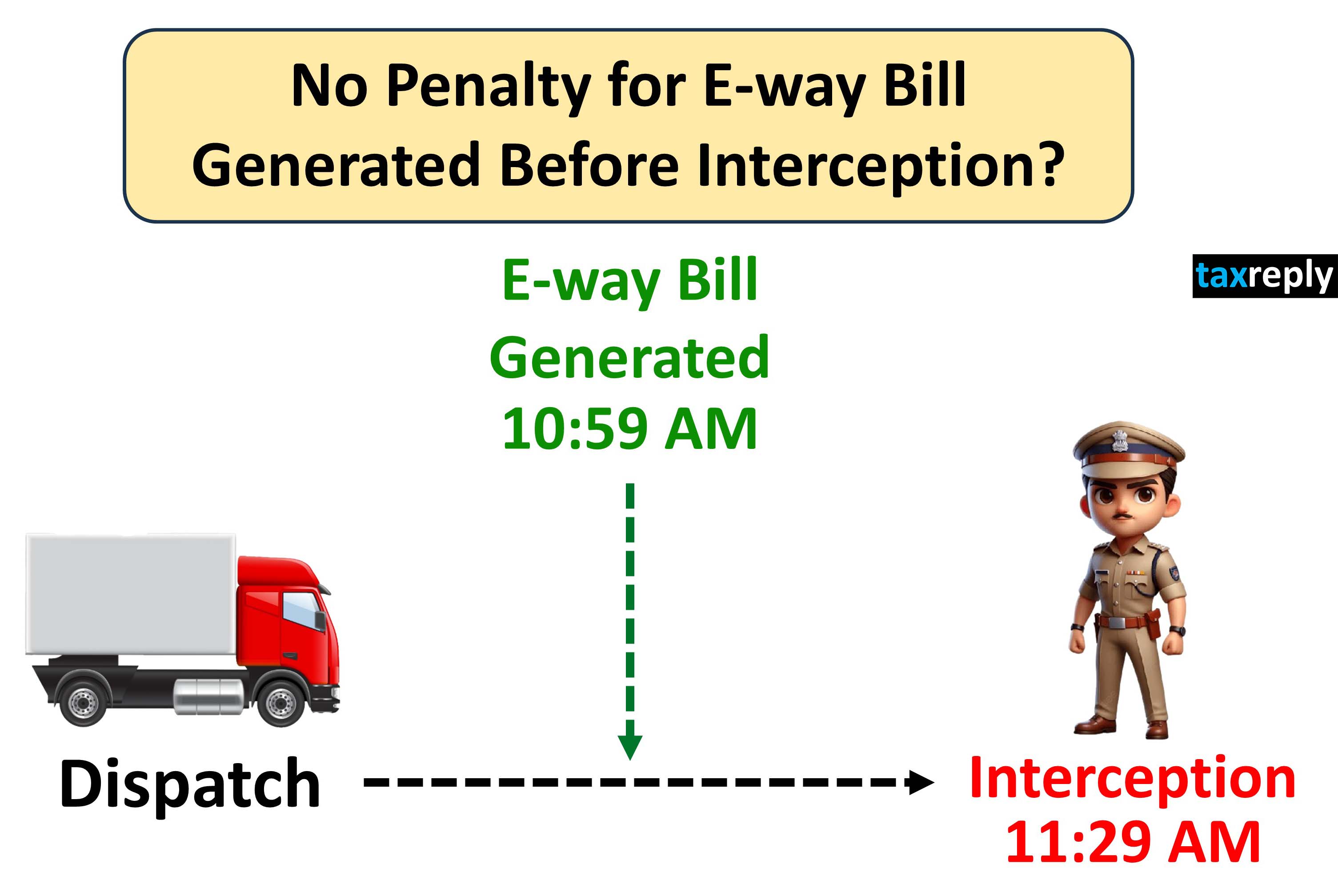

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.68k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|