®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

10.45k

10.45k

Cases when e-way bill is not required

Rule 138 of CGST Rules

Generation of e-way bill

E-way bill is required for every movement of goods (whether inter-state or intra-state) where value of goods exceeds Rs. 50,000.

However below are some exceptions / exemptions where e-way is not required even if the value of goods exceeds Rs.50,000.

Exceptions to e-way bill - Rule 138(14) of CGSR Rules

(a) where the goods being transported are specified in annexure. View Annexure

(b) where the goods are being transported by a non-motorised conveyance (also known as human powered transportation e.g. cycle, rickshaw, hand carts, horse carts, skates, carrying goods in hands or on shoulders etc.)

(c) where the goods are being transported

from the customs port, airport, air cargo complex and land customs station

to an inland container depot or a container freight station

for clearance by Customs;

(d) in respect of movement of goods within such areas as are notified under clause (d) of sub-rule (14) of rule 138 of the State or Union territory Goods and Services Tax Rules in that particular State or Union territory;

(e) where the goods (except de-oiled cake) are specified in the Notification No. 2/2017- Central tax (Rate) dated 28th June, 2017 as amended from time to time. View Notification No. 2/2017 and all further amendments to the same

(f) where the goods being transported are -

- alcoholic liquor for human consumption,

- petroleum crude,

- high speed diesel,

- motor spirit (commonly known as petrol),

- natural gas or

- aviation turbine fuel

(g) where the supply of goods being transported is treated as no supply under Schedule III of the Act. View Schedule III of CGST Act

(h) where the goods are being transported—

(i) under customs bond from an inland container depot or a container freight station to a customs port, airport, air cargo complex and land customs station, or from one customs station or customs port to another customs station or customs port, or

(ii) under customs supervision or under customs seal.

(i) where the goods being transported are transit cargo from or to Nepal or Bhutan;

(j) where the goods being transported are exempt from tax under -

- notification No. 7/2017-Central Tax (Rate), dated 28th June 2017 as amended from time to time View Notification No. 7/2017 and all further amendments to the same

- notification No. 26/2017- Central Tax (Rate), dated the 21st September, 2017 as amended from time to time View Notification No. 26/2017 and all further amendments to the same

(k) any movement of goods caused by defence formation under Ministry of defence as a consignor or consignee.

(l) where the consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail.

(m) where empty cargo containers are being transported.

(n) where the goods are being transported upto a distance of twenty kilometers for weighment

- from the place of the business of the consignor to a weighbridge or

- from the weighbridge back to the place of the business of the said consignor

subject to the condition that the movement of goods is accompanied by a delivery challan issued in accordance with rule 55.

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 2 Jun, 2018 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Comments

Jun 9, 2020

department issued notice regarding Input E-way bill supplies not match in GSTR-1 and GSTR-3B. if manufacture how to maintain inward e-way bill and matching.

please give your opinion or any case laws. whether need to give or not.

May 12, 2022

Post your comment here !

|

Login to Comment

|

Other Important Updates

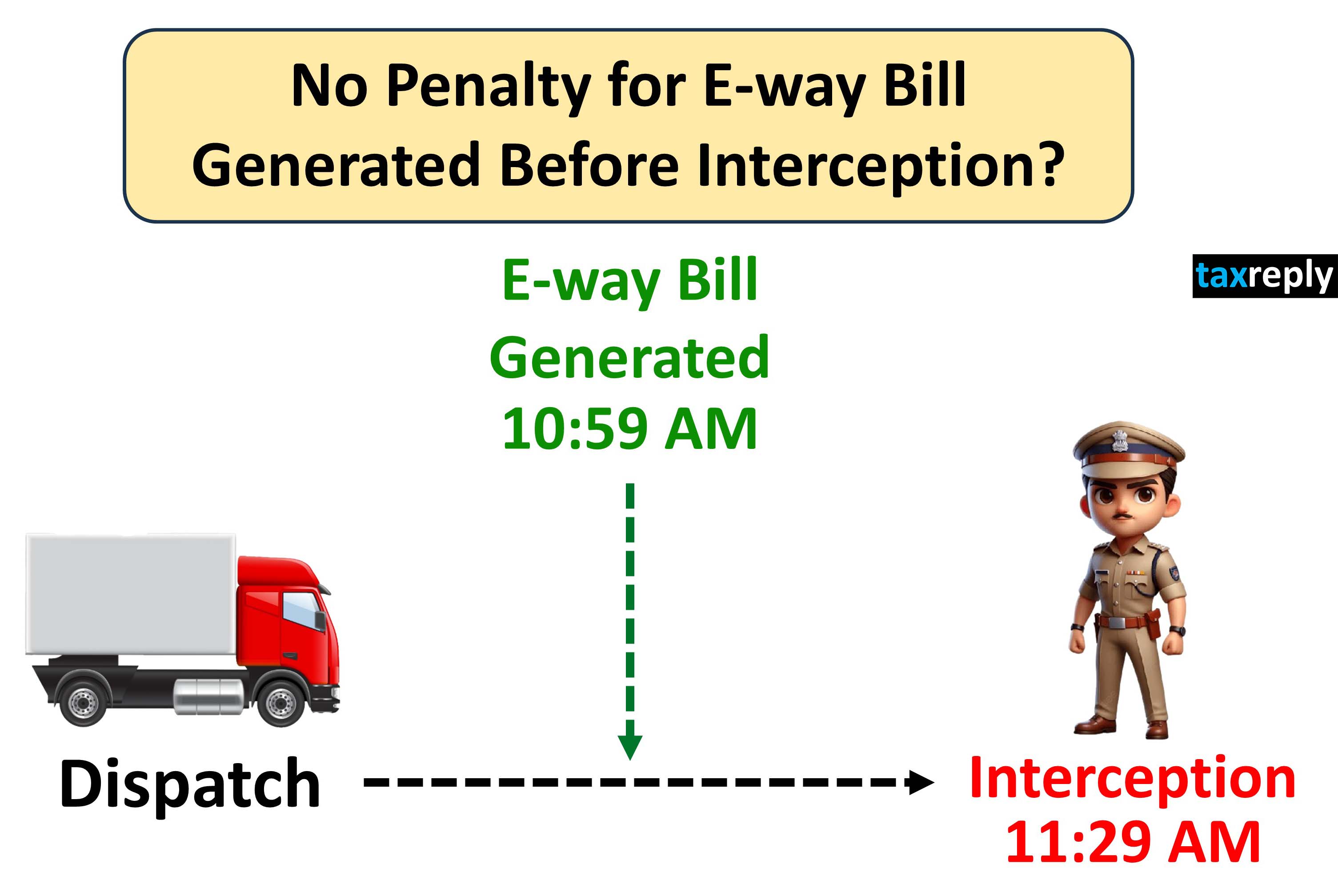

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.63k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|