®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

4.14k

4.14k

Proposed improvements in e-way bill generation, being released on 16.11.2018

1. Checking of duplicate generation of e-way bills based on same invoice number

The e-way bill system is enabled not to allow the consignor/supplier to generate the duplicate e-way bills based on his one document. Here, the system checks for duplicate based on the consignor GSTIN, document type and document number. That is, if the consignor has generated one e-way bill on the particular invoice, then he will not be allowed to generate one more e-way bill on the same invoice number. Even the transporter or consignee is not allowed to generate the e-way bill on the same invoice number of that consignor, if already one has been generated by the consignor.

Similarly, if the transporter or consignee has generated one e-way bill on the consignor’s invoice, then any other party (consignor, transporter or consignee) tries to generate the e-way bill, the system will alert that there is already one e-way bill for that invoice, and further it allows him to continue, if he wants.

2. CKD/SKD/Lots for movement of Export/Import consignment

CKD/SKD/Lots supply type can be used for movement of the big consignment in batches. When One ‘Tax Invoice’ or ‘Bill of Entry’ is there, but the goods are moved in batches from supplier to recipient with the ‘Delivery Challan’, then this option can be used. Here, the batch consignment will have ‘Delivery Challan’ along with copy of the ‘Tax Invoice’ or ‘Bill of Entry’ in movement. The last batch will have the ‘Delivery Challan’ along with original ‘Tax Invoice’ or ‘Bill of Entry’.

Some exports or imports will be in big consignment and may not be moved in one go from the supplier or to the recipient. Hence, CKD/SKD/Lots supply can be used for this.

For CKD/SKD/Lots of Export consignment, the ‘Bill To’ Party will be URP or GSTIN of SEZ Unit with state as ‘Other Country’ and shipping address and PIN code will be of the location (airport/shipping yard/border check post) from where the consignment is moving out from the country.

For CKD/SKD/Lots of Import consignment, the ‘Bill From’ Party will be URP or GSTIN of SEZ Unit with state as ‘Other Country’ and dispatching address and PIN code will be of the location (airport/shipping yard/border check post) from where the consignment is entered the country.

3. Shipping address in case of export supply type

For Export supply type, the ‘Bill To’ Party will be URP or GSTIN of SEZ Unit with state as ‘Other Country’ and shipping address and PIN code will be of the location (airport/shipping yard/border check post) from where the consignment is moving out from the country.

4. Dispatching address in case of import supply type

For Import supply, the ‘Bill From’ Party will be URP or GSTIN of SEZ Unit with state as ‘Other Country’ and dispatching address and PIN code will be of the location (airport/shipping yard/border check post) from where the consignment is entered the country.

5. ‘Bill To – Ship To’ transactions

There are four types of ‘Bill To – Ship To’ transactions. These types depend upon the number of parties involved in the billing and movement of the goods. The following paras explain the same.

o Regular: This is a regular or normal transaction, where Billing and goods movement are happening between two parties - consignor and consignee. That is, the Bill and goods movement from consignor to consignee takes place directly.

o Bill To – Ship To: In this type of transaction, three parties are involved. Billing takes places between consignor and consignee, but the goods move from consignor to the third party as per the request of the consignee.

o Bill From – Dispatch From: In this type of transaction also, three parties are involved. Billing takes places between consignor and consignee, but the goods are moved by the consignor from the third party to the consignee.

o Combination of both: This is the combination of above two transactions and involves four parties. Billing takes places between consignor and consignee, but the goods are moved by the consignor from the third party to the fourth party, as per the consignee’s request.

6. Changes in Bulk Generation Tool

New columns have been added in the Bulk Generation Tool. The same will be released on 16th November 2018.

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 14 Nov, 2018 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Post your comment here !

|

Login to Comment

|

Other Important Updates

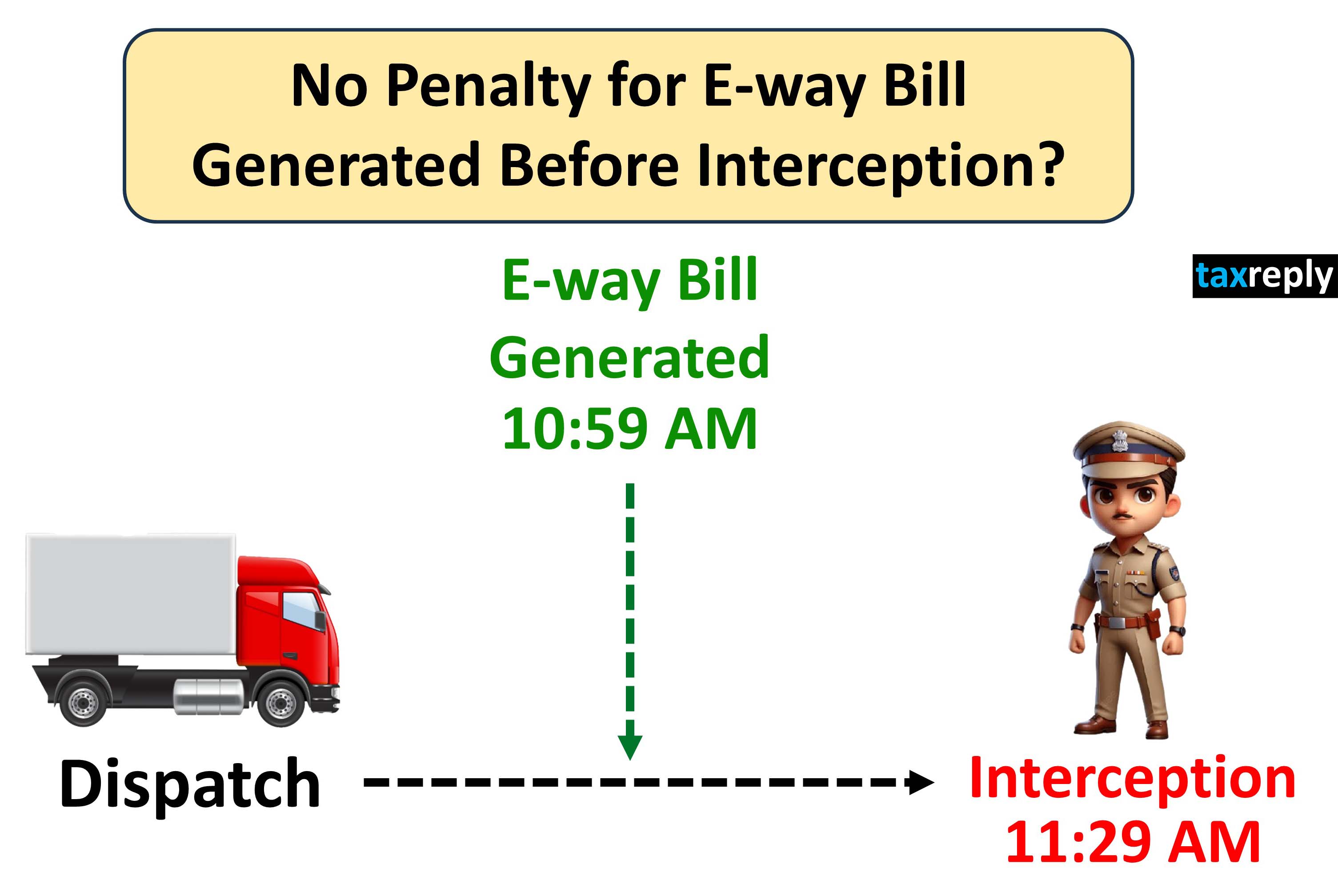

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.63k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|