®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

17.55k

17.55k

Penalty for not carrying e-way bill during transportation of goods -

Section 122(1)(xiv) of CGST Act

Penalty for certain offenses

Where a taxable person who transports any taxable goods without the cover of documents as specified (e.g. e-way bill), he shall be liable to pay a penalty of Rs.10,000 or an amount equivalent to the tax evaded, whichever is higher.

Therefore minimum penalty for not carrying the e-way bill shall be Rs.10,000.

Reference - Section 122 of CGST Act

Section 129(1) of CGST Act

Detention, seizure and release of goods and conveyance in transit

Where any person transports any goods or stores any goods (in transit) in contravention of the provisions of this Act or the rules made thereunder, all such goods and conveyance shall be liable to detention or seizure. After detention or seizure, it shall be released on payment of below amount -

Where the owner of the goods comes forward for payment of tax and penalty:

-

In case of Taxable goods - Applicable tax on such goods + Penalty equal to 100% of the tax payable on such goods.

- In case of Exempted goods - 2% of value of goods or Rs.25,000, whichever is less

Where the owner of the goods does not come forward for payment of tax and penalty:

-

In case of Taxable goods - Applicable tax on such goods + Penalty equal to 50% of the value of goods reduced by the tax amount paid thereon

- In case of Exempted goods - 5% of the value of goods or Rs.25,000, whichever is less,

Reference - Section 129 of CGST Act​

Section 122(3)(b) of CGST Act

Penalty for certain offenses

Any person who acquires possession of, or in any way concerns himself in transporting, removing, depositing, keeping, concealing, supplying, or purchasing or in any other manner deals with any goods which he knows or has reasons to believe are liable to confiscation under this Act or the rules shall be liable to a penalty which may extend to twenty-five thousand rupees.

Reference - Section 122 of CGST Act

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 1 Jun, 2018 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Comments

Dec 28, 2022

Jun 2, 2024

Post your comment here !

|

Login to Comment

|

Other Important Updates

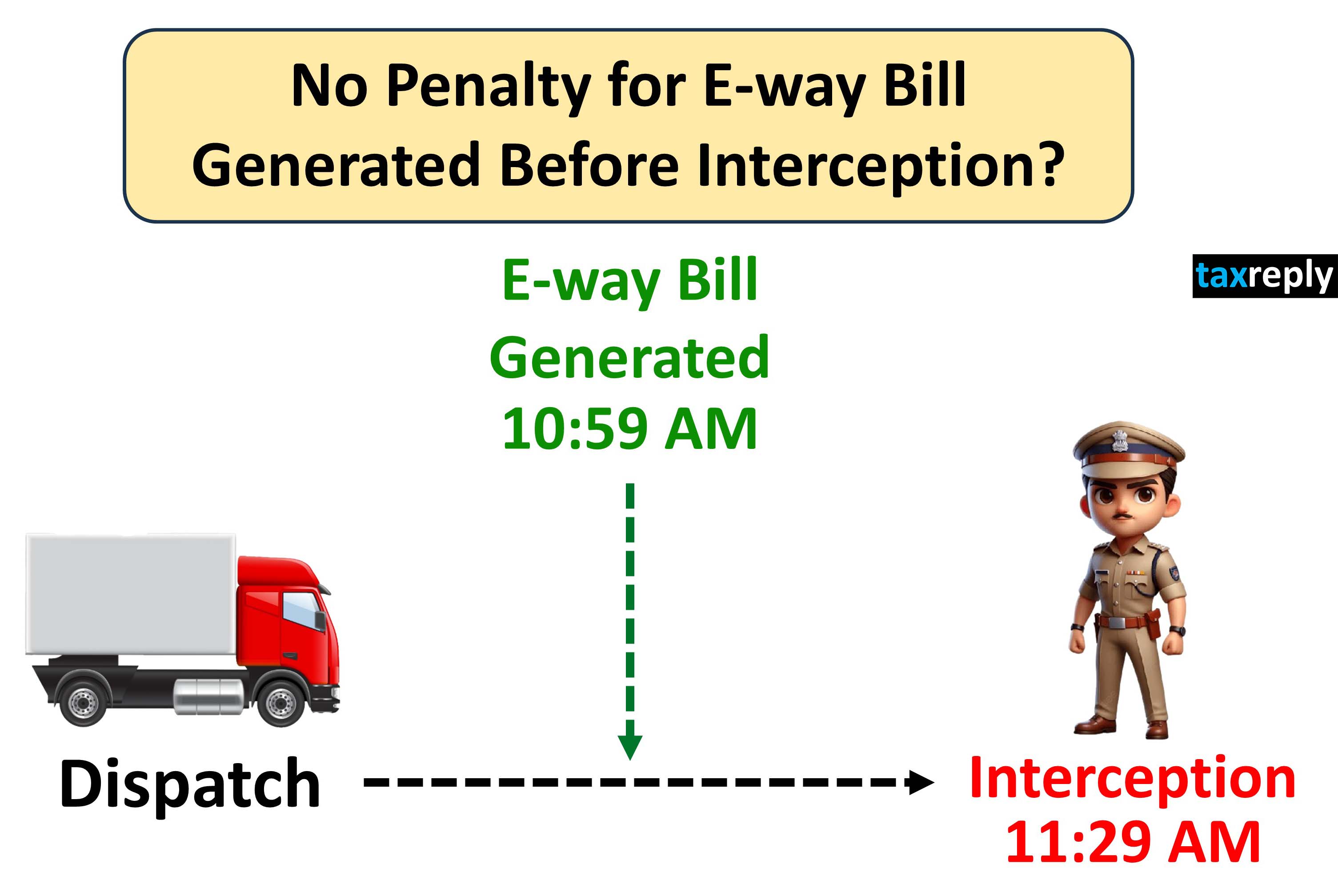

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.57k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|