®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

4.45k

4.45k

Notification No. 41/2020 - Central Tax dated 05.05.2020

CBIC extended the due date for furnishing of annual return (GSTR-9 & GSTR-9C) for the financial year 2018-2019 till the 30th September, 2020.

Notification extracted below.

NOTIFICATION

No. 41/2020–Central Tax

G.S.R. 275(E).—In exercise of the powers conferred by sub-section (1) of section 44 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act), read with rule 80 of the Central Goods and Services Tax Rules, 2017 (hereafter in this notification referred to as the said rules), and in supersession of notification No. 15/2020-Central Tax, dated the 23rd March, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 198(E), dated the 23rd March, 2020, except as respects things done or omitted to be done before such supersession, the Commissioner, on the recommendations of the Council, hereby extends the time limit for furnishing of the annual return specified under section 44 of the said Act read with rule 80 of the said rules, electronically through the common portal, for the financial year 2018-2019 till the 30th September, 2020.

******

Notification No. 40/2020 - Central Tax dated 05.05.2020

Validity of e-way bills expiring between 20.03.2020 to 15.04.2020 has been extended to 31st May 2020.

Notification extracted below.

NOTIFICATION

No. 40/2020–Central Tax

G.S.R. 274(E).—In exercise of the powers conferred by section 168A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act), read with section 20 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017), and section 21 of Union Territory Goods and Services Tax Act, 2017 (14 of 2017), the Central Government, on the recommendations of the Council, hereby makes the following amendment in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No.35/2020- Central Tax, dated the 3rd April, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i), vide number G.S.R. 235(E), dated the 3rd April, 2020, namely:- In the said notification, in the first paragraph, in clause (ii), the following proviso shall be inserted, namely: - ―Provided that where an e-way bill has been generated under rule 138 of the Central Goods and Services Tax Rules, 2017 on or before the 24th day of March, 2020 and its period of validity expires during the period 20th day of March, 2020 to the 15th day of April, 2020, the validity period of such e-way bill shall be deemed to have been extended till the 31st day of May, 2020.

******

Notification No.39/2020 - Central Tax dated 05.05.2020

- Corporate Debtors who has filed thier all GST Returns before appointment of IRP/RP are not required to follow special procedure as specified vide Notification No. 11/2020 - Central Tax dated 21.03.2020.

- New registration to be obtained within 30 days of appointment of IRP/RP or 30.06.2020, whichever is later.

NOTIFICATION

No. 39/2020–Central Tax

G.S.R. 273(E).—In exercise of the powers conferred by section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Government, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No.11/2020- Central Tax, dated the 21st March, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number

G.S.R. 194(E), dated the 21st March, 2020, namely:—

In the said notification

-

in the first paragraph, the following proviso shall be inserted, namely: -

―Provided that the said class of persons shall not include those corporate debtors who have furnished the statements under section 37 and the returns under section 39 of the said Act for all the tax periods prior to the appointment of IRP/RP.‖;

-

for the paragraph 2, with effect from the 21st March, 2020, the following paragraph shall be substituted, namely: -

―2. Registration.- The said class of persons shall, with effect from the date of appointment of IRP / RP, be treated as a distinct person of the corporate debtor, and shall be liable to take a new registration (hereinafter referred to as the new registration)in each of the States or Union territories where the corporate debtor was registered earlier, within thirty days of the appointment of the IRP/RP or by 30th June, 2020, whichever is later.

******

Notification No. 38/2020 - Central Tax dated 05.05.2020

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 5 May, 2020 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Comments

May 6, 2020

May 6, 2020

Post your comment here !

|

Login to Comment

|

Other Important Updates

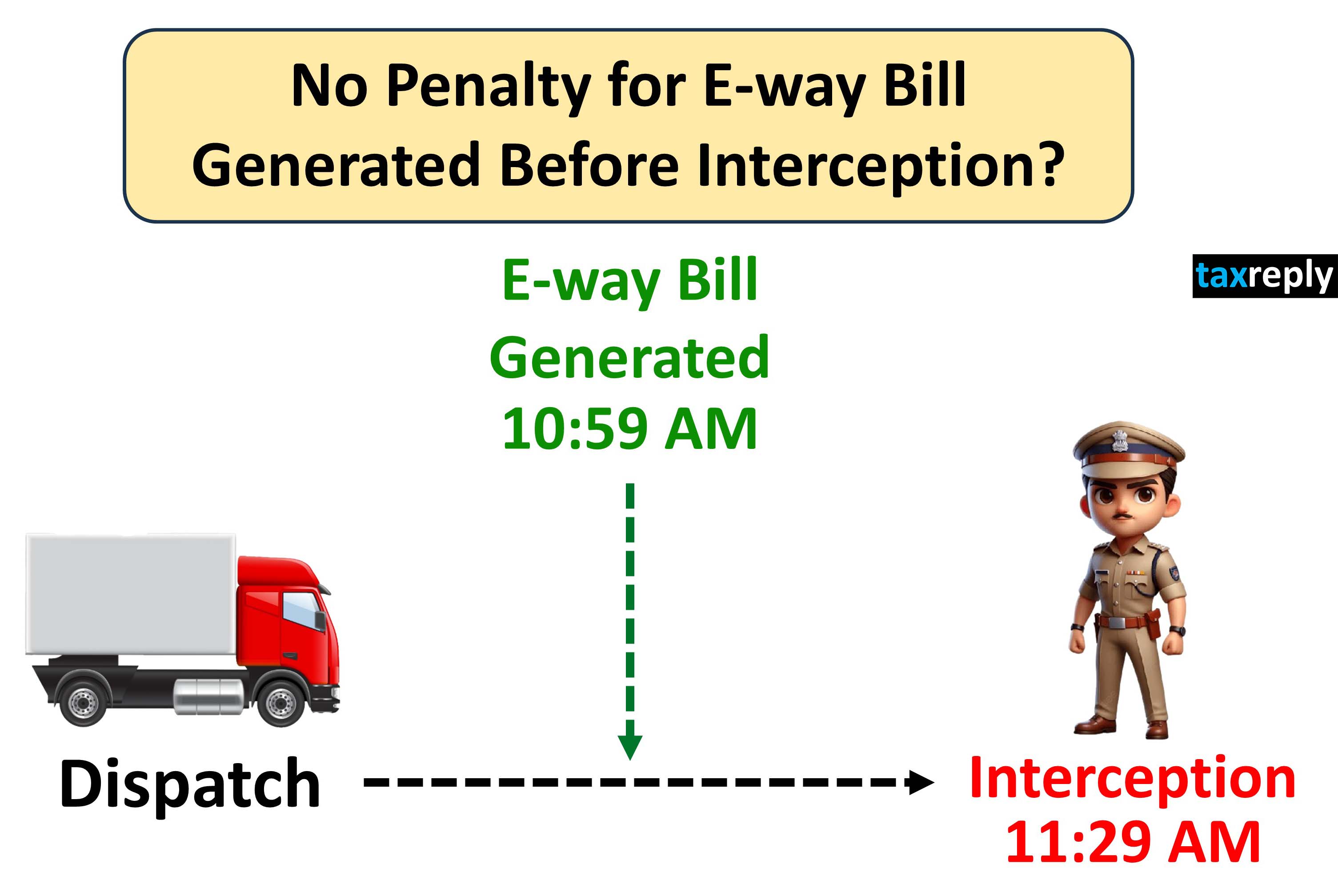

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.68k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|