®

®

TaxReply India Private Limited

GST Library Plans

Best GST Library

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

(From 22.09.25)

GST Rates

(Upto 21.09.25)

HSN Codes

GST Forms

My Favourites

GST Diary

GST Notebook

GST Staff Manager

GST Fees Manager

GST Login Tool

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

1 Jan, 1970 05:30 AM

1 Jan, 1970 05:30 AM

6.02k

6.02k

Centre vs. State E-way Bill?

Taxpayer was fined by the State, for carrying Central E-way bill instead of State E-way bill: High Court set aside the order

|

The whole basis, based upon which the order has been passed that the petitioner was not carrying the E-way bill as required under the U.P. G.S.T. Rules, looses significance as the petitioner were not liable to be taxed under the U.P. G.S.T. Act being an inter-state supply. - High Court |

Petitioner:

The present petition has been filed challenging the order passed by Adjudicating Authority under the U.P. G.S.T. Act imposing tax and penalty on petitioner for non-compliance of e-way bill.

The petitioner is a dealer registered under GST in the State of UP.

Petitioner made a supply of 25 batteries vide Tax Invoice dated 26.02.2018. It is clear that while raising an Invoice, the petitioner had levied and deposited IGST at the rate of 28%.

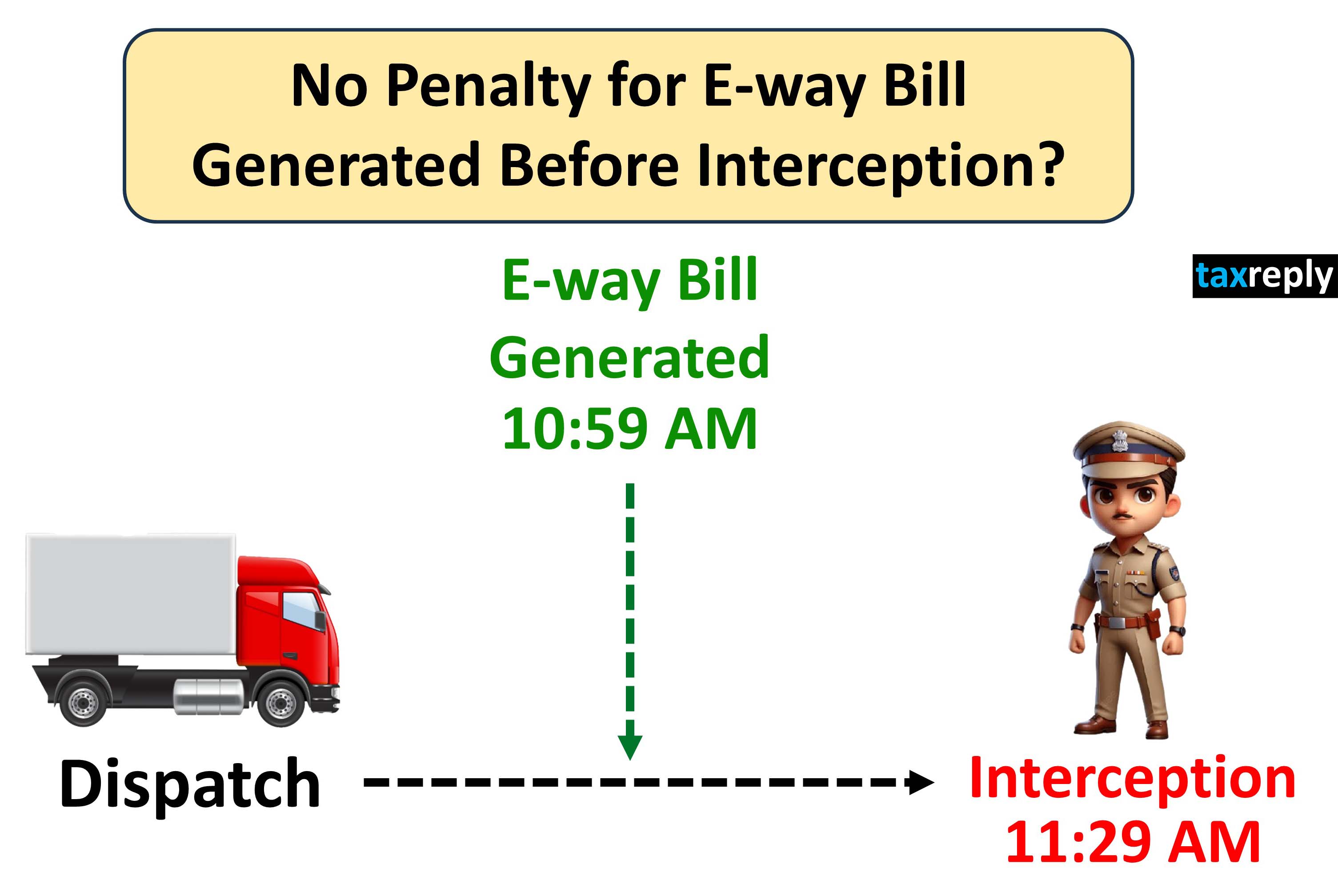

The petitioner for obtaining E-way bill, uploaded prescribed details on the portal of the G.S.T. and generated the E-way bill for the goods in question. It is stated that the details of dispatched goods were also entered on the portal and the same was also printed on the E-way bill.

It is stated that when the goods reached at Lucknow, it was intercepted by Mobile Squad of the Commercial Tax Department on 08.03.2018 and a seizure order in purported exercise of powers under Section 129(1) of the U.P. G.S.T. Act was passed on 08.03.2018. The reason as recorded for passing the seizure order was that the E-way bill system, as introduced by the Central Government under the CGST, was replaced by the State E-way bills, which had been suspended by the Central Government w.e.f. 02.02.2018. Thus, the State was of the view that once the Central Government had suspended its E-way bill, the requirement of the State E-way bill stood revived automatically and as the petitioner was not carrying the State E-way bill, the seizure order came to be passed.

Revenue:

Learned Standing Counsel on the other hand argues that in pursuance to the circular issued by the State Government, as contained in Annexure-1, wherein directions were issued that the provisions of mandatory E-way bill stood revived from the night of 09.02.2018 and directions were issued for taking steps to check the violations thereof, the State Authorities were justified in passing the order, as admittedly the petitioner did not have the G.S.T. bill as was required under the provisions of U.P. G.S.T. Act and the Rules framed thereunder. He, thus, prays that the writ petition is liable to be dismissed.

Held by High Court:

Listen Full Case in Simple Words

|

☛ Login to read more...

|

| Author |

CA Mohit Jain |

| Qualification | Chartered Accountant, M.Com |

| Experience | 15+ Years Experience in Taxation |

| Mobile | (+91) 8383842726 |

| mohit@taxreply.com | |

| Published on | 2 Aug, 2022 |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

Post your comment here !

|

Login to Comment

|

Other Important Updates

No Penalty for E-way Bill Generated after Dispatch of goods but before Interception by GST Officers: High Court

18 Nov 2025

12.68k

Section 73 vs 74: High Court remitted back the matter to GST Authorities to examine whether proceedings were rightly initiated under Section 74 instead of Section 73

14 Nov 2025

10.93k

Time limit for filing GST Appeal in Section 107(4) is not strictly mandatory: High Court

13 Nov 2025

4.23k

Department cannot deny Buyer's ITC solely due to subsequent cancellation of Supplier GST Registration: High Court Rules

12 Nov 2025

9.5k

Can GST Department start recovery proceedings immediately after expiry of appeal window without waiting for condonation period?

11 Nov 2025

9.81k

No interest can be levied from the date of deposit of amount in Electronic Cash Ledger till the actual filing of GSTR-3B: High Court Held

10 Nov 2025

4.7k

GST Notices and Orders without Physical Signature are Valid if uploaded through Digital Keys of Officer: High Court Holds

9 Nov 2025

3.97k

|

☛ Read more updates...

|